|

implications for business owners.

implications for business owners.

|

|

|

When it comes to maintaining motorcoaches and fleet vehicles, one of the most common tax questions we see is:

Should this expense be deducted now—or capitalized over time?

At BUSBooks, we work closely with clients in the transportation and motorcoach industry, and this distinction can have a meaningful impact on your tax position and cash flow.

Understanding the Difference

The IRS separates vehicle-related costs into two categories:

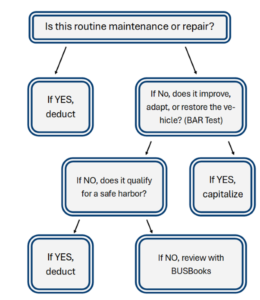

A Simple Framework: The “BAR” Test

To determine how an expense should be treated, we apply the IRS “BAR” test:

If the answer to any of these is “yes,” the cost must be capitalized.

Common Examples

Generally Deductible:

Generally Capitalized:

Opportunities to Maximize Deductions

Several IRS safe harbors may allow you to deduct costs that might otherwise be capitalized:

Why This Matters

Proper classification:

How BUSBooks Can Help

We don’t just prepare returns—we help you make informed decisions throughout the year. If you’re planning significant repairs or upgrades to your vehicles, we recommend discussing them with us in advance so we can help you optimize the tax treatment.

Our Repairs vs. Capitalization checklist and decision tree is included below and may help you determine if you need additional assistance. If you have questions about a recent or upcoming expense, we’re here to help.

Repairs vs. Capitalization Decision Tree

Repairs vs. Capitalization Checklist

Step 1: Identify the Expense

☐ What work was performed?

☐ Is it routine or a major upgrade?

Step 2: Apply the BAR Test

Betterment

☐ Fixes a defect that existed before purchase

☐ Improves performance, efficiency, or quality

☐ Adds a significant new component

Adaptation

☐ Changes the vehicle for a new or different use

Restoration

☐ Replaces a major component (engine, transmission, HVAC)

☐ Rebuilds the vehicle to like-new condition

☐ Repairs after major damage

If ANY box is checked → Capitalize

Step 3: If NOT an Improvement

☐ Keeps vehicle in normal operating condition

☐ Is routine or recurring maintenance

☐ Does not extend useful life

If YES → Deduct as Repair

Step 4: Check Safe Harbors

☐ Under $2,500 per item (De Minimis Safe Harbor)

☐ Recurring maintenance expected multiple times

☐ Within small taxpayer limits

30-Second Takeaway

30-Second Takeaway

Operator Perspective

Before I was part of a CPA Firm serving the motorcoach industry, I spent 30 years as a motorcoach operator. Like many of you, I watched fuel prices swing wildly over the years—sometimes slowly, and sometimes overnight.

When fuel moves quickly, margins can disappear just as fast. The cycle has returned.

The Industry Has Rebuilt

Over the past few years, the motorcoach industry has done something remarkable. It rebuilt itself. When COVID shut down group travel, coaches across the country were parked. Charter work disappeared overnight. Companies that had spent decades building their businesses suddenly found themselves fighting simply to survive. But this industry has always been resilient.

Operators tightened expenses, protected their fleets, kept key employees, and waited for travel to return. And return it did. Today operators are experiencing one of the strongest demand environments the industry has seen in years. Schools are traveling again. Domestic tour groups are back. Sports teams and corporate groups have returned to the road. The international tourism market has collapsed, but that is another story. For many companies, the industry has entered a welcome period of renewed prosperity. But experienced operators also know something else about this business.

Good times can stop quickly by forces outside the industry’s control – a sudden surge in fuel prices.

Why the Iran Conflict Matters

The recent escalation of tensions in the Middle East—particularly involving Iran—has introduced uncertainty into global oil markets. Oil is traded globally. Even though the United States produces a substantial portion of its own energy, prices still respond quickly to geopolitical risk. When instability appears in major oil-producing regions, markets react almost immediately. Even the possibility of disruptions to production or shipping routes can push prices higher.

For diesel-dependent industries like motorcoach transportation, those reactions show up quickly at the pump. Unlike labor costs, insurance premiums, or maintenance expenses, fuel prices can change dramatically in a brief period. And when they do, the impact on operating margins is immediate.

Fuel Surcharges Are Nothing New

Fortunately, the transportation industry has dealt with this before. Fuel surcharges have been used across trucking, airlines, and passenger transportation for more than two decades. Whenever fuel prices spike—as they did in the mid-2000s, during the 2008 oil surge, and again during the diesel increases in 2022—transportation providers rely on surcharges to manage rapidly rising fuel costs.

The reason is simple. Trips and contracts are often priced months in advance. Fuel prices can move dramatically in a matter of weeks and even days. Fuel surcharges help bridge that gap. They allow operators to maintain their base pricing while adjusting for extraordinary fuel increases in a transparent and predictable way. Most customers already understand the concept because they see it regularly on airline tickets and freight shipments.

Operators Are Already Feeling Cost Pressure

Fuel volatility is arriving at a time when motorcoach operators are already facing rising costs. Insurance premiums across the industry have been climbing steadily. Liability coverage has become more expensive, and many operators have experienced significant increases in annual premiums. Insurance increases are difficult, but they usually happen gradually. Fuel costs behave very differently. They can rise quickly—and when they do, they move far faster than insurance costs.

A typical coach traveling about 100,000 miles per year may consume more than 10,000 gallons of diesel annually. A $1.00 increase in diesel prices adds an approximate $10,000 in annual fuel cost for that single coach. A $2.00 increase adds $20,000 annual increase per coach – a fleet of twenty coaches will sustain a drain of $400,000 to the bottom line.

While insurance increases are already squeezing margins, fuel increases can outpace those pressures overnight.

How High Could Diesel Go?

Another question operators should consider is how high diesel prices could climb. In parts of the country, diesel prices are already reaching levels that would have seemed extreme only a few years ago. In California, diesel is already approaching $7.00 per gallon in certain markets. If global oil markets tighten further, prices could climb much higher. In a severe supply disruption, $10 diesel at the pump is not a dream. For companies running multiple coaches every day, that kind of increase cannot simply be absorbed.

Example Fuel Surcharge Structure Operators Can Use

Many operators ask what a simple surcharge structure might look like. Below is a straightforward example commonly used in transportation:

Baseline Diesel Price:

$4.00 per gallon

Adjustment:

For every $0.25 increase above the baseline, apply a surcharge.

Average Diesel Price Fuel Surcharge

$4.00 or less No surcharge

$4.25 2%

$4.50 4%

$4.75 6%

$5.00 8%

$5.25 +10%

Again, this is a simple example. Many companies reference the U.S. Energy Information Administration (EIA) weekly diesel price index when applying fuel surcharges. Using a public index helps keep the process transparent and easy to explain to customers.

Final Thoughts

Final Thoughts

Motorcoach operators have always been problem solvers. This industry has navigated recessions, fuel cycles, regulatory changes, and even a global shutdown. The recovery we are seeing today is proof of that resilience. But protecting that recovery requires staying ahead of potential risks. If diesel prices continue rising quickly, operators who implement fuel surcharges early will be in a far stronger position than those who wait.

At BUSBooks.cpa, we work exclusively with motorcoach companies and understand the financial realities unique to this industry. Helping operators identify financial risks early and respond proactively is an important part of what we do. The motorcoach industry has already overcome enormous challenges. With thoughtful planning, it can navigate this one as well.

From Peter Shelbo of BUSBooks, LLC